The Markets in Crypto-Assets Regulation (MiCA) is a crucial component of the European Commission's digital finance strategy. This regulation will take effect for electronic money token issuers on June 30, 2024, and for crypto-asset service providers (CASPs) on December 30, 2024. This means that these cryptocurrency service providers will need to comply with new regulatory requirements.

MiCA covers many crypto-assets that were previously outside the scope of EU financial services legislation, categorizing them into three types: asset-referenced tokens (ARTs), electronic money tokens (EMTs), and other crypto-assets. This classification will determine how these assets are regulated, ensuring that investors receive appropriate protection.

In this article, Ouxin will provide a detailed analysis of the main aspects of MiCA and its impact on the industry. We will discuss licensing requirements, preparation work, DORA and digital finance, EBA technical standards and guidelines, and MiCA's future outlook for the entire cryptocurrency industry.

Types of Crypto-Assets Covered by MiCA

1. Asset-Referenced Tokens (ARTs)

Asset-referenced tokens (ARTs) are crypto-assets whose value is stabilized by referencing other assets or rights, including one or more official currencies. The goal of ARTs is to provide stable value, similar to traditional currencies or commodities. The regulatory requirements for these tokens include:

Transparency and Disclosure: Issuers must provide investors with detailed disclosures, explaining their stabilization mechanism, reference assets, custody arrangements, and holders' rights.

Capital and Reserve Requirements: Issuers must maintain sufficient reserve assets to support the token's value stability and ensure these assets are strictly separated from the issuer's own assets.

Governance and Risk Management: Issuers must establish sound governance structures and risk management systems, including business continuity plans and internal control mechanisms.

2. Electronic Money Tokens (EMTs)

Electronic money tokens (EMTs) are crypto-assets whose value is stabilized by referencing only one official currency, similar to traditional electronic money. These tokens are typically used for payments and transactions. The regulatory requirements for EMTs include:

Issuer Authorization: EMT issuers must obtain authorization as an electronic money institution or credit institution, ensuring their operations comply with the relevant requirements of the Electronic Money Directive (EMD II).

Redemption Rights: Holders have the right to redeem their electronic money tokens at any time at the face value of the reference currency, and issuers must clearly state this right in the white paper.

Funds and Liquidity: Issuers must maintain sufficient liquidity and fund reserves to meet redemption demands and ensure the safety and availability of funds.

3. Other Crypto-Assets

Other crypto-assets include all crypto-assets that do not fall under ARTs or EMTs, such as utility tokens. These assets are typically used to access specific services or products rather than as a means of payment. The regulatory requirements for these tokens include:

White Paper Requirements: Issuers must prepare and submit a white paper to the competent authorities, providing detailed information about the issuer, project, technology, and risks.

Market Abuse Prevention: Issuers and service providers must take measures to prevent market abuse, including insider trading and market manipulation.

Transparency and Compliance: Issuers must ensure their operations are transparent and comply with relevant compliance requirements, including anti-money laundering and customer identification (KYC/AML) procedures.

Companies engaged in crypto-asset activities need to carefully assess their business to determine whether they qualify as "crypto-assets" under MiCA. If the crypto-assets do not meet MiCA's definition, they may need to comply with other existing financial regulations, such as the Electronic Money Directive (EMD II), Payment Services Directive (PSD II), or the Markets in Financial Instruments Directive II (MiFID II) for transferable securities.

MiCA Licensing Requirements

MiCA establishes new requirements for entities intending to provide services related to crypto-assets. These entities should be established in an EU country and obtain the relevant license from national competent authorities (such as credit institutions, electronic money institutions, investment companies, and other financial market participants). This change in regulatory bodies will significantly impact all CASPs registered in the EU, as in some jurisdictions, different institutions are responsible for regulating such companies (e.g., tax authorities and financial intelligence units). A unified approach will undoubtedly improve regulation of the industry and allow for the implementation of EU standards in this field, similar to the regulation of other financial market participants, guided by the European Banking Authority and the European Securities and Markets Authority. MiCA requires CASPs to obtain authorization (license) in their country of establishment. The main application requirements are as follows:

Local Substance Requirements

CASPs should have at least one senior management member (director) located in the country of establishment and organize activities through a business location within the EU. This approach allows for appropriate regulation.

Provision of Financial Services Norms

CASPs will be regarded as providers of financial services within the meaning of EU legislation, and therefore certain consumer protection rules will apply to their clients. Crypto-asset service providers should provide clients with clear, fair, and non-misleading information and warn them about the risks associated with crypto-assets.

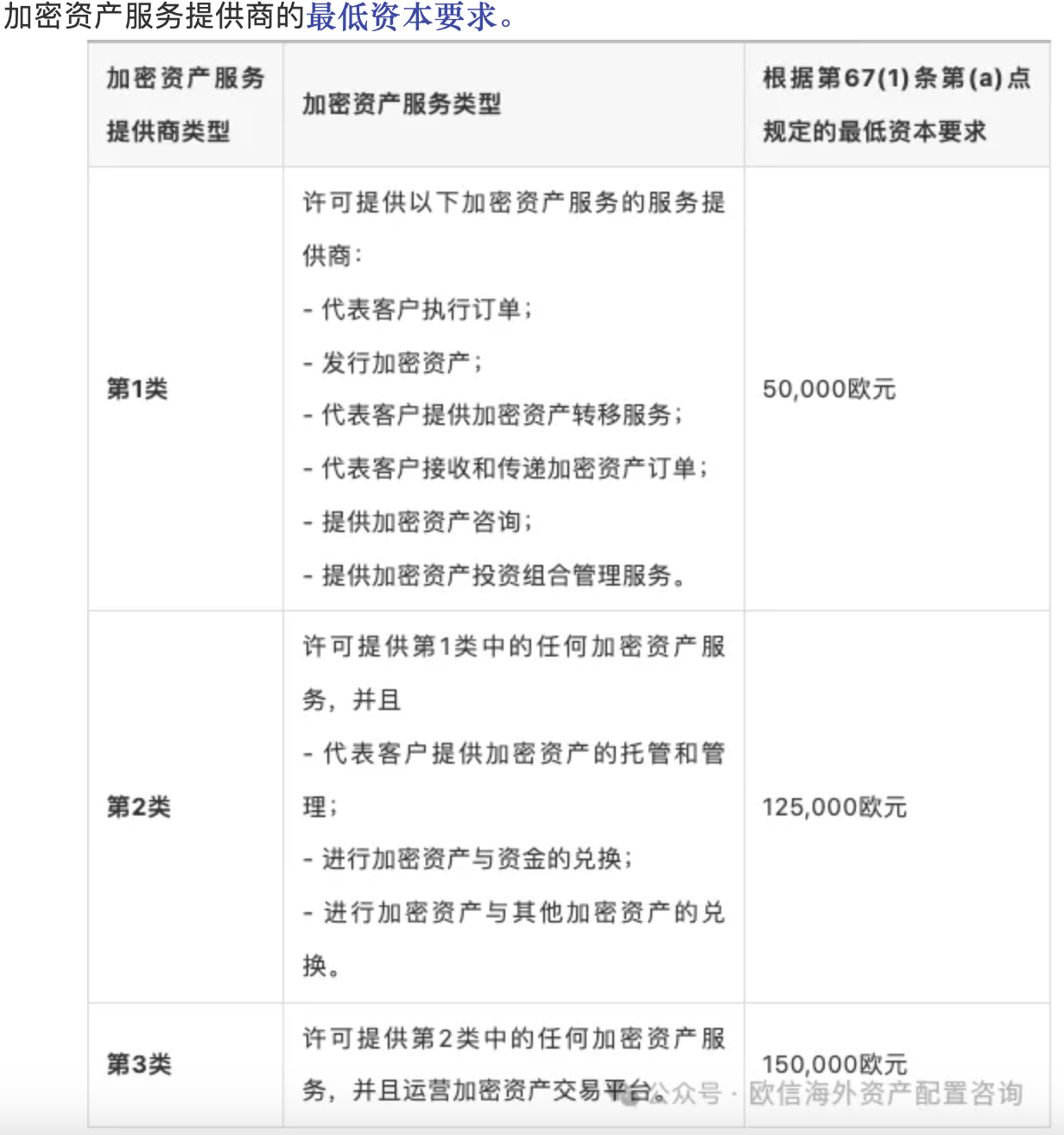

Capital Requirements

MiCA sets minimum capital requirements for CASPs, ranging from 50,000 euros to 150,000 euros, while establishing own funds monitoring requirements similar to those for other financial market participants.

Requirements for UBOs, Shareholders, Senior Management, and Employees

CASPs, beneficial owners, shareholders, and senior management should have a good reputation and be fit to engage in anti-money laundering and counter-terrorism financing activities. In controlling this situation, regulatory authorities will be able to consult with each other within the EU (including financial intelligence units).

CASPs should also employ management and staff with sufficient skills, knowledge, and professional competence and take all reasonable measures to perform their functions appropriately. They should demonstrate the ability to devote sufficient time to effectively execute their duties.

Internal Policies and Governance Principles Requirements

MiCA sets requirements for the internal processes of CASPs, making them similar to other regulated financial institutions. This approach requires the development of certain policies in areas such as anti-money laundering/counter-terrorism financing, data protection, risk management, consumer protection, safeguards, business continuity, and conflict of interest avoidance. Additionally, the new regulation requires certain types of CASPs to comply with rules previously applicable to investment companies to prevent market abuse, disorderly trading conditions, and other behaviors that may infringe on user rights.

Transition Period for Existing CASPs

For existing CASPs in the EU, an 18-month transition period has been established, allowing them to continue providing services within 18 months after full application in December 2024, until July 1, 2026, or until they obtain or are denied MiCA authorization. However, member states have the option to appropriately shorten the transition period. For example, Ireland and Poland have provided a 12-month transition period for CASPs, Italy has provided 10 months, and France has provided an 18-month transition period.

Passporting and Solicitation of Foreign Clients

MiCA establishes an EU passporting system for CASPs, allowing them to provide services to the entire EU market while being established and having an office in only one jurisdiction (similar to electronic money institutions, investment companies, etc.).

CASPs Commencement of Operations and Continuity Requirements

CASPs should commence their business activities within 12 months of receiving approval and are prohibited from ceasing operations for more than 9 months while holding an active license.

Application Preparation

The European Securities and Markets Authority (ESMA) released a consultation paper on MiCA in July 2023, outlining the key requirements for a successful application.

Companies that have already obtained authorization generally do not need to reapply for authorization under MiCA, provided they meet certain disclosure requirements, including notifying their member state regulatory authorities of the crypto-asset services they intend to provide.

1. Disclosure Requirements

- Transparency: All crypto-asset service providers (CASPs) and issuers must provide detailed disclosure information to investors and regulatory authorities. This includes business models, risk factors, financial conditions, and other important information that may affect investor decisions.

- White Paper: For new crypto-asset issuances, issuers need to prepare a white paper detailing the project's technology, use, risks, governance structure, and funding use. The white paper must be filed with the relevant regulatory authorities.

2. Anti-Money Laundering (AML) Rules

- Customer Due Diligence (CDD): CASPs need to conduct strict identity verification and due diligence on all customers to prevent money laundering and terrorist financing activities. This includes verifying customer identities, monitoring transaction activities, and regularly updating customer information.

- Reporting Obligations: CASPs must regularly report suspicious activities to regulatory authorities and comply with all reporting obligations required by AML regulations.

3. Governance Requirements

- Management Structure: CASPs need to establish sound governance structures to ensure efficient and transparent management. This includes the composition of the board, division of responsibilities among management, and internal control mechanisms.

- Risk Management: CASPs need to develop and implement comprehensive risk management policies covering market risk, credit risk, operational risk, and legal risk.

4. Licensing Procedures

- Application and Approval: All CASPs wishing to operate in the EU must submit a license application to the competent authorities of the member state where their registered office is located. The application must include detailed information on the business plan, governance structure, risk management policies, and financial condition.

- Compliance Review: Competent authorities will conduct a comprehensive review of the application to ensure the applicant meets all MiCA requirements. Upon approval, CASPs will receive a license to operate within the EU.

DORA and Digital Finance

As a core component of the European Commission's digital finance strategy, MiCA aims to provide a comprehensive regulatory framework for the digital finance ecosystem within the EU. This strategy also includes a new regulation on Digital Operational Resilience (DORA) and a new regulation on a Distributed Ledger Technology (DLT) pilot regime.

DORA (Digital Operational Resilience Act), as part of the MiCA strategy, aims to ensure that all financial institutions, including crypto-asset service providers (CASPs), have sufficient resilience in the face of various digital operational risks.

The DLT (Distributed Ledger Technology) pilot regime aims to promote the development of financial market infrastructure based on distributed ledger technology DLT.

EBA Technical Standards and Future Outlook

The European Banking Authority (EBA) has issued a series of technical standards and guidelines on prudential matters under the MiCA regulation, focusing on the core prudential elements of the crypto-asset industry: own funds, liquidity requirements, and recovery plans. The development of these new standards aims to strengthen market regulation of crypto-assets while building a more structured and rigorous prudential framework for financial institutions within the EU.

Through MiCA, DORA, and the DLT pilot regime, the EU digital finance strategy is committed to establishing a secure, transparent, and innovative financial ecosystem. The joint implementation of these regulations not only aims to create a safer, more transparent, and continuously innovative financial ecosystem but also lays a solid foundation for future digital financial innovation by ensuring the healthy development of the crypto-asset market, enhancing investor and user confidence.

In summary, MiCA is not only an independent regulatory framework but also an important part of the EU digital finance strategy. As these new regulations are gradually implemented, we look forward to seeing the rise of a more regulated, transparent, and vibrant EU digital finance market, bringing positive and far-reaching impacts to the global financial market.

That's all for today's sharing. Welcome to follow the public account: Ouxin_Consulting or leave a comment in the comment section to exchange and discuss with me.

About Ouxin Ouxin Overseas Asset Allocation Consulting Company is an international consulting company established in Europe, mainly assisting clients in the UK, Ireland, Portugal, Lithuania, Malta, and other countries with services including overseas fund establishment, overseas financial license application, overseas company establishment, overseas bank account opening, overseas real estate investment, and second identity planning.

Currently, the company can assist clients in applying for major financial licenses including: Forex broker licenses, electronic banking licenses, payment licenses, fund licenses, offshore trust licenses, and digital currency licenses.