Currently, time is becoming increasingly important. Quickly entering the market means you can have more time than your peers to understand and capture the market.

However, Europe's complex financial regulations and regulatory systems indeed cause headaches for most people.

The increase in time costs means you might lose the first-mover advantage.

"White label" can help you quickly solve this problem.

NO. 1|One

What is White Label

In simple terms, a "white label" is purchasing a standard "solution." While you cannot change the core functions of the solution, such as service and product content, compliance management, etc., you can change the brand's logo and user interface.

In the Fintech field, a white label refers to a licensed company packaging its licenses, system infrastructure, backend support, human resources, etc., into a solution and leasing it to a third party.

This way, the third party can provide related services by leveraging the license, enjoying a complete operational system of the licensed company without any construction costs, thus better focusing on their brand development.

Unlike ordinary agents, companies choosing white labels focus more on operating their brand.

Ordinary agents merely act as intermediaries between the license holder and customers to introduce and promote the licensed company's services or products.

Therefore, compared to ordinary agents, white labels are more independent and can develop a customer base with their business philosophy, making them more suitable for Fintech companies planning to hold their licenses in the future.

NO. 2|Two

Benefits of White Label

Saves time costs: No need to prepare cumbersome application materials or go through lengthy approval processes.

Saves operational costs: Applicants can precisely know the cost of establishing a white label company and subsequent operational expenses.

(No need to develop an independent IT infrastructure, website maintenance, legal advisors, or hire licensed personnel with relevant qualifications, etc.)

Focus more on business development, brand promotion, and marketing: The white label provider, i.e., the host licensed company, will solve all backend operations and compliance issues for you.

Stay up-to-date and timely updates: The host licensed company already has a complete backend system, only needing to be updated to keep up with the times, reducing labor and time costs.

More flexible agreement model: In the white label service agreement, the revenue and cost model is more flexible. You can customize the price and fee structure for providing services without being constrained by the host licensed company.

Overall, white label companies can receive various technical support and compliance assistance without bearing the significant responsibilities of a licensed company themselves.

NO. 3|Three

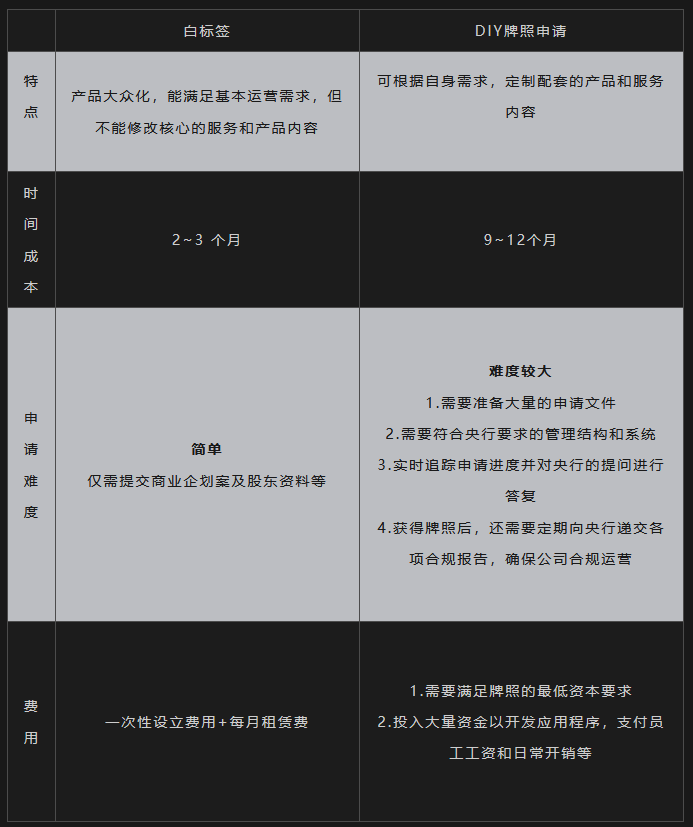

White Label vs. DIY License Application

Comparison Overview

In conclusion:

In fact, both white label and DIY license applications have their merits, and you should choose according to your needs.

However, OuXin believes that white labels are more suitable for startups that are just beginning and want to enter the fintech industry.

Because white labels can help companies quickly enter the market and save costs. The unique content of the company can be gradually improved as the company matures. Regulatory agencies are also more likely to accept this gradually improving business model.

DIY licenses are more inclined towards companies with a clear plan for their brand and market. These companies often have a more complex organizational structure and a more distinctive brand. This uniqueness can help them stand out in the fintech field.

That's all for today's sharing. Feel free to leave comments and discuss with me in the comment section.

About OuXin

OuXin Overseas Asset Allocation Consulting Company is an international consulting company established in Europe, mainly assisting clients in the UK, Ireland, Portugal, Lithuania, Malta, and other countries with services including overseas fund establishment, overseas financial license application, overseas company establishment, overseas bank account opening, overseas real estate investment, and second identity planning, etc.

Currently, the company can assist clients in applying for financial licenses, including: Forex broker licenses, electronic banking licenses, payment licenses, virtual currency trading licenses, and ICO virtual currency issuance licenses.