Oushin Consulting Oushin Overseas Asset Allocation Consulting 1 week ago

Think back, how long did it take you to get a bank card last time?

Ten minutes? Half an hour?

Imagine if it took you more than an hour to get a card at a bank in China, wouldn't you complain?

But let me tell you, if in Europe, any bank can get you a bank card within an hour, you should definitely give them a banner of appreciation.

Take Ireland as an example, whether you are applying for a personal or business account, it is a very cumbersome process:

① Appointment: Whether for a personal or business account, you need to make an appointment with the bank first, this requires the customer to wait 1-2 weeks

② Face-to-face meeting: After the appointment, the bank will schedule a time with you, and you need to bring all the materials to the bank. (Note: Your materials must be correct, and you must arrive on time, otherwise the bank will not process your application. If you want to continue, the bank will schedule another appointment, which means another 1-2 weeks of waiting);

③ Card collection: After completing all the above steps, you also need to wait 5-10 business days to successfully open an account. This does not include the time for mailing the bank card, and the bank card, PIN, and account information will be sent in 3 separate mails.

Due to the cumbersome operations of traditional banks, electronic banking is ushering in its spring in Europe.

01.

The pandemic prompts European consumers to shift to cashless payments

The COVID-19 pandemic swept across the globe at lightning speed, becoming the greatest challenge humanity has faced since World War II. However, such global "black swan events" inevitably have dual effects.

After the pandemic, the global economic and social landscape will accelerate towards digitalization, intelligence, and health, with the electronic payment industry being the most deeply affected.

In 2020, the European Central Bank conducted a survey, in which 40% of respondents said they reduced their use of cash since the pandemic, and 87% said they intend to maintain this habit even after the pandemic ends.

In 2017, the volume of electronic payment transactions in Europe was approximately $668 billion, but just two years later, in 2019, electronic payments grew by nearly 33%, with transaction volumes exceeding $887 billion.

With the advent of the COVID-19 pandemic, 2021 saw explosive growth in European electronic payments, increasing by over $270 billion in one year. According to professional assessments, by 2025, European electronic payments will grow by another $775 billion, surpassing the entire electronic payment transaction volume of Europe in 2017.

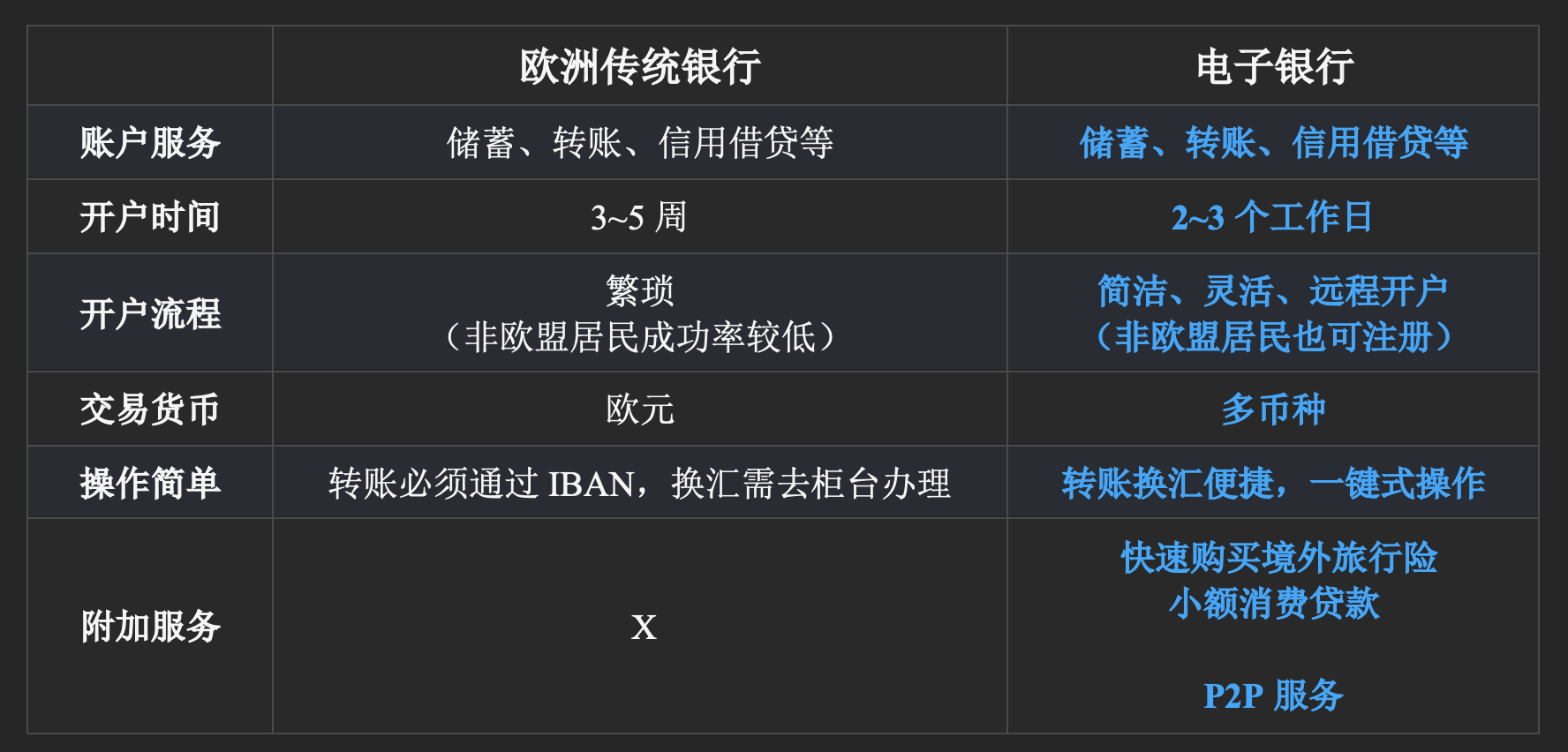

Although electronic banks need to rely on the underlying physical banks for fund custody, electronic banks are capturing more European consumers with their unique advantages:

Electronic banks (EMI) can do much more than basic activities like currency exchange and transfers. They can also offer many other services, such as trading in precious metals like gold and silver, and support for trading in highly recognizable virtual currencies (such as Bitcoin, Litecoin, etc.).

Electronic banks (EMI) can do much more than basic activities like currency exchange and transfers. They can also offer many other services, such as trading in precious metals like gold and silver, and support for trading in highly recognizable virtual currencies (such as Bitcoin, Litecoin, etc.).

02.

European electronic payments are in full bloom

①Revolut—The European "Alipay" captures the hearts of Chinese people

In recent years, Revolut has been quite popular in the UK and Europe, especially among the Chinese community, as if realizing the dream of using Alipay abroad!

Here are some of Revolut's advantages summarized for your reference.

① A single account can open multiple foreign currency accounts for free, with up to 30 currencies available;② Currency exchange between various foreign currency accounts under the same account can be done at a super favorable real-time exchange rate, with instant credit;

③ Real-time monitoring of exchange rate changes in the app, set app alerts at your ideal exchange rate point for instant currency exchange;

④ Without leaving home, purchase overseas travel insurance with one click, and at a price better than the market;

⑤ Provides real-time transaction information and virtual account services (accounts are automatically destroyed after one use) to safeguard transaction security.

②Transferwise—One-click cross-border transfers

Transferwise's currency exchange feature is also often praised. As an electronic bank, it fundamentally differs from Revolut. Revolut leans towards currency exchange for personal use, while Transferwise specializes in international transfers to others. For example, transferring your euro account savings to your parents' RMB account or Alipay in China.

① Supports currency transfers in over 40 countries;

② Utilizes the best real-time exchange rates, with fees lower than traditional banks;

③ Achieves international transfers with instant credit.

③Stripe, Sumup, etc.—Empowering small and micro enterprises with online payments

With the outbreak of the pandemic, almost all merchants in Europe began accepting mobile payments, and the local e-commerce and cross-border e-commerce industries in Europe have rapidly grown like mushrooms after rain. Whether offline or online, merchants need to choose a payment gateway, but traditional payment gateways are generally controlled by physical banks, with expensive annual fees and stringent application conditions, making it difficult for small and micro enterprises to apply. Stripe, Sumup, and other institutions with electronic banking licenses seized this opportunity, lowering the usage threshold for small and micro enterprises.

① Low application threshold, and many are exempt from monthly fees, making it easy for small catering and taxi industries to apply;

② Low cost, with a portable card reader available for just a few euros, or you can directly install a mobile app.

It is worth mentioning that the founders of Stripe are Irish child prodigies, the brothers John and Patrick. They started their entrepreneurial journey before the age of 16, and when they founded Stripe, Patrick was only 21 and John was only 19. In 2016, John became the world's youngest self-made billionaire.

According to a Bloomberg report in March 2021, Stripe's current valuation is $95 billion, exceeding any bank in the Eurozone. This shows that the electronic payment industry has also gained favor from the capital market and recognition of its potential.

It is evident that the development of electronic banks in Europe is full of vitality, unlike the Chinese market, which is dominated by WeChat Pay and Alipay. At that time, the European market, its electronic banking and electronic payment industry were still in their infancy, full of opportunities and infinite possibilities.

03.

What is an electronic banking license

But how can you establish an electronic banking institution? First, you need to have an electronic banking license. So what services can an electronic banking license provide? Here, Oushin helps you sort them out:

① Open payment accounts for clients (including businesses and individuals), provide cash deposit and withdrawal services, and related account services;

② Provide payment services to third parties for clients (including businesses and individuals), including remittances, bank transfers, online payments, and e-commerce online collections, credit card loan payments, or foreign exchange, etc.;

③ Issue Visa or Mastercard debit and credit cards for clients (including businesses and individuals);

④ Provide small consumer loan services for clients (including businesses and individuals);

⑤ Issue stable electronic currency based on blockchain.

Additionally, many electronic banks in the EU will apply for some additional small licenses to better provide comprehensive services to clients, such as offering P2P business and insurance services, etc.

More importantly, an electronic banking license applied for in any EU country can be used to provide the above services throughout the EU via the EU passport.

04.

The application process and time for an electronic banking license

The application time for an electronic banking license varies depending on the country of application. Although it is the same set of EU regulations, different regulatory bodies have their own requirements in execution.

The fastest approval can be completed in 3 months, while the slowest may take a year or longer. Oushin Consulting will recommend the most suitable country for application based on the client's needs, helping clients obtain the key to open the market in the shortest time.

The application process is as follows:

① Oushin's consulting team meets with the client. Based on the client's business model and goals, we create a tailored application plan for the client. This includes introducing specific application requirements, establishing a suitable corporate structure, and suggesting the optimal application country;

② Oushin represents the client to contact relevant service providers, including local law firms, custodian banks, insurance companies, audit firms, and IT system suppliers, and helps the client review relevant service agreements. Ensuring cooperation with highly credible enterprises without adding unnecessary service items;

③ Oushin's consulting team helps the client draft relevant application materials. This includes business plans, company operation documents, financial budgets, risk assessments, and related company management charters;

④ After submitting the preliminary application materials, the central bank will provide the first round of feedback. Oushin's consulting team will respond to the central bank's inquiries on behalf of the client. If necessary, we will also attend meetings with the central bank on behalf of the client;

⑤ After receiving the response, the central bank will conduct a second review and provide feedback. Similarly, Oushin's team will assist the client in responding and providing the required supplementary materials;

⑥ After receiving all feedback and approving the application, the central bank will issue the electronic banking license.

Undoubtedly, electronic payments have driven rapid and transformative development in the entire financial and technology industries. The world is currently undergoing a major transformation from a traditional economy to a digital economy, and as the digital transformation of enterprises accelerates in the future, regulation will inevitably become increasingly stringent in the coming years.

Oushin Consulting helps clients seize the best opportunity of the moment to gain a market entry advantage. Allowing clients to focus on business expansion without any worries.

That's all for today's sharing. Feel free to leave a comment and discuss with me in the comment section.

About Oushin

Oushin Overseas Asset Allocation Consulting Company is an international consulting firm established in Europe, primarily assisting clients in the UK, Ireland, Portugal, Lithuania, Malta, and other countries, including overseas fund establishment, overseas financial license application, overseas company establishment, overseas bank account opening, overseas real estate investment, and second identity planning.

Currently, the company can assist clients in applying for the following financial licenses:Forex broker licenses, electronic banking licenses, payment licenses, virtual currency trading licenses, and ICO issuance of virtual currency licenses.